Toronto Income Property Newsletter: July 2012

Happy Canada Day everyone! I hope that you are all enjoying your long weekend and are looking forward to taking some more time off this summer. It’s going to be hot out there so try to stay cool. We live in great province with plenty to do so make sure you take advantage of it.

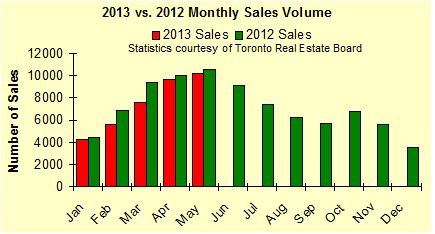

The real estate market always slows down during these summer months. I have been hearing talk lately about a little dip in the Toronto market, but honestly it is too early to tell if this is true. I know that there aren’t enough duplexes and triplexes out there for my existing buyer base (so what else is new?). Until I see cap rates go back up to five and a half and a healthy selection of investment inventory in all downtown areas that doesn’t trade immediately, then I might say that the market is starting to turn. Not yet though … I still think that it is the warm weather and the most productive agents (who do 95% of the business) are taking it a little easier.

To all my Italian and Spanish friends: Enjoy the big game today. It should be a classic.

Flaherty Changes Mortgage Rules

This past month, finance minister Jim Flaherty announced new tougher mortgage lending rules. The government will no longer guarantee insured mortgages with terms exceeding twenty five years. They also lowered the maximum amount that Canadians can borrow against the value of their homes, from 85% to 80% when refinancing. They also removed federal backing for home equity lines of credit, (HELOCs) which have become increasingly popular over the past couple of years. Lastly, CMHC will no longer apply to purchases over a million dollars. This last one is a no-brainer to me. Why has the government been assisting borrowers who can afford million dollar homes?

The purpose of these changes is to slow down the pace of real estate activity overall and to keep high risk borrowers in check. The lower amortization requirements are a good thing as I believe that 30 and 40 year amortizations make it very difficult for folks to quickly pay down their mortgages. Given the record levels of household debt, I think this move was intended to keep average Canadians from getting even deeper into debt. In the free-for-all that happened in the USA four years ago it is a shame that the government there didn’t introduce similar measures to keep unqualified borrowers from getting in over their heads. A senior economist at TD bank suggests that the amortization change could affect as many as 20,000 home sales per year.

“We want to make sure we don’t have the kind of medium-term problem that has been experienced elsewhere because of this tendency by some to assume large indebtedness at low interest rates,” Mr. Flaherty said. “People need to demonstrate that good Canadian trade of prudence and reasonableness in terms of their debt assumptions.”

Avery Shenfeld, my economics professor form my U of T days had this to add: “These latest steps to tighten mortgage rules are part of efforts to avoid the negative side effects of having very low interest rates for a long time”.

Bank of Canada governor Mark Carney hasn’t raised interest rates so these new rules may buy him a little more time before he may have to deal with the inevitable. Interest rates can’t stay this low forever. People who have been saving their money may be less ahead of folks who have leveraged to the nines to buy property to increase their net worth. Logically this shouldn’t be the case, but with five years of historic low lending rates, this has become the new reality.

2012 Q1 Rental Market

The Toronto real estate Board reported 3,804 leased condominium apartment transactions in the first quarter of 2012, up 11 per cent from the 3,442 units rented during the first three months of 2011. The number of condominium apartments listed for rent on the TorontoMLS system during the first quarter was also up, but by a lesser four per cent to 7,096 units. Now while there are no statistics available for suites in duplexes, triplexes and multiplexes, these figures give us some keen insight as to what is happening with rentals.

“There have been very few purpose-built rental buildings completed in the GTA over the past few years. This means that households looking to rent an apartment with modern finishes and amenities have been focusing on condominium apartments rented out by investor owners,” said Toronto Real Estate Board President Richard Silver.

“Condominium apartment vacancy rates, as reported by CMHC, were down in 2011 and it looks as if this trend is continuing with growth in lease transactions outstripping growth in listings,” continued Silver.

Average one-bedroom and two-bedroom condominium apartment rents increased at annual rates above inflation, at four and seven per cent respectively.

“Tighter rental market conditions played a key role in the strong annual average rent increases. However, a lot of condominium apartment projects were completed over the last year. Some owners chose to list their units for rent. Newly completed units benefitting from the latest trends in finishes and amenities could have arguably commanded higher rents compared to older units. This factor likely played a role in strong year-over-year average rent increases as well,” said Jason Mercer, TREB’s Senior Manager of Market Analysis.

In all my years in the investment property business I have never know the rental market to be soft. That is why it is always a prudent move to look at buying income generating properties in the GTA.